Many brokers who we are talking to see NCCP compliance documents as something that ‘just has to be done’ to maintain their accreditations and avoid fines. NCCP Act was introduced to offer national consumer credit protection. Consumers deserve and have a right to be informed about who are they dealing with, what is the impact of the credit and who is getting paid as a result of credit provision to them. Unfortunately, documentation can be cumbersome and it will often (if not treated properly) create obstacles in the sales process.

Typical errors we see

- Too many documents ‘offloaded’ to the customer without a proper explanation what do these really represent;

- NCCP documents are longer than they should be;

- Documents lack graphics and are written using heavy legal terminology;

- Documents lack all actual fees that the borrower will be paying;

- Documents don’t represent actual pre and post loan financial status;

- Documents require signatures where acknowledgement is not really necessary, etc.

Imagine this scenario

You are getting a loan and your broker has just asked you to sign the Privacy Statement (Privacy Act requirement) and given you a credit guide. During the interview, your broker collects your ID, proof of income, savings statements, contacts/rates notices and few more documents necessary to compete loan application. Before leaving, your broker asks you to complete and email a 10+ pages long Fact Find document that is also necessary to complete the application form.  Within couple of days you are presented with the loan options, and once you pick the preferred product your broker sends you preliminary assessment and credit proposal disclosure documents. Next you receive a 10-page loan application form, which you have to sign in 2-3 places as well. They also ask you for some additional documents specifically required by this lender. Well, you are receiving a free service, but you are already bombarded by 6-7 different documents, multiple signature requests and have spent few hours in meetings, photocopying, scanning, completing and signing forms. The last thing you want to hear at this stage is that once your loan application is submitted, you are about to be swamped with further explanation requests and documents from your chosen lender during the process that can take several weeks to complete. How likely are you to be satisfied with such service, refer others or repeat business with the broker?

Within couple of days you are presented with the loan options, and once you pick the preferred product your broker sends you preliminary assessment and credit proposal disclosure documents. Next you receive a 10-page loan application form, which you have to sign in 2-3 places as well. They also ask you for some additional documents specifically required by this lender. Well, you are receiving a free service, but you are already bombarded by 6-7 different documents, multiple signature requests and have spent few hours in meetings, photocopying, scanning, completing and signing forms. The last thing you want to hear at this stage is that once your loan application is submitted, you are about to be swamped with further explanation requests and documents from your chosen lender during the process that can take several weeks to complete. How likely are you to be satisfied with such service, refer others or repeat business with the broker?

The alternative

Dealing with multiple aggregator platforms, we can see the best practice in each of these areas. It is possible to reduce size of NCCP documents. Signatures are rarely required to prove that documents were prepared and presented. People generally prefer graphics to text and don’t really read anything longer than two pages. Most documents can be filled on line, on a PDF and not longer two to three pages at any time. The best brokers take their clients on a journey, explain timeframes and process carefully and they utilise all the necessary compliance documents in their sales tools. We see that these brokers get referred and repeat business all the time. All it takes is to rethink your compliance document design, your initial and ongoing approach in communicating these to your clients.

Examples and suggestions:

Examples and suggestions:

- A single, combined privacy collection statement and credit guide document.

- Two part Fact Find – one with all the personal/employment details, assets, liabilities and expenses and the other with the responsible lending elements. Broker can fill the second document after the interview leaving the borrowers to complete a two page fillable PDF on their PC.

- Combined preliminary assessment and credit proposal disclosure document, with a graphic representation of preferred and compared products and clearly stated fees payable by the borrower.

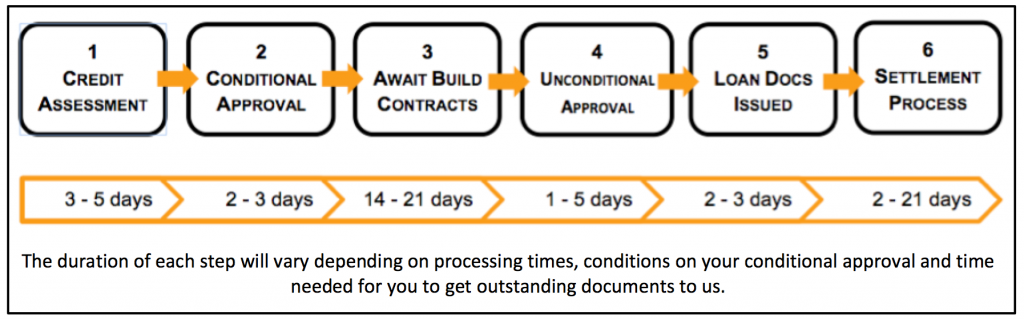

- Graphically explained credit process, detailing expected lender actions and timeframes (eg picture above).

- Use of electronic signatures to minimise printing, scanning and emailing of documents.

Contact us if you would like to receive examples of these documents.